How Catastrophic Injury Cases Differ From Standard Claims

Most people think personal injury cases work the same way regardless of how badly someone gets hurt. You file a claim, the insurance company argues about it, and eventually there’s a settlement or maybe a trial. That’s the basic shape these cases take.

But when an accident causes a catastrophic injury, everything changes. These aren’t just “bigger” versions of standard claims. The legal standards are different. The evidence bar sits higher. The money involved reaches entirely different levels.

When someone suffers a severe fall on unsafe property that causes permanent harm, slip and fall injury lawyers face challenges that go beyond what routine injury cases demand—the entire legal approach shifts.

Defining the Dividing Line

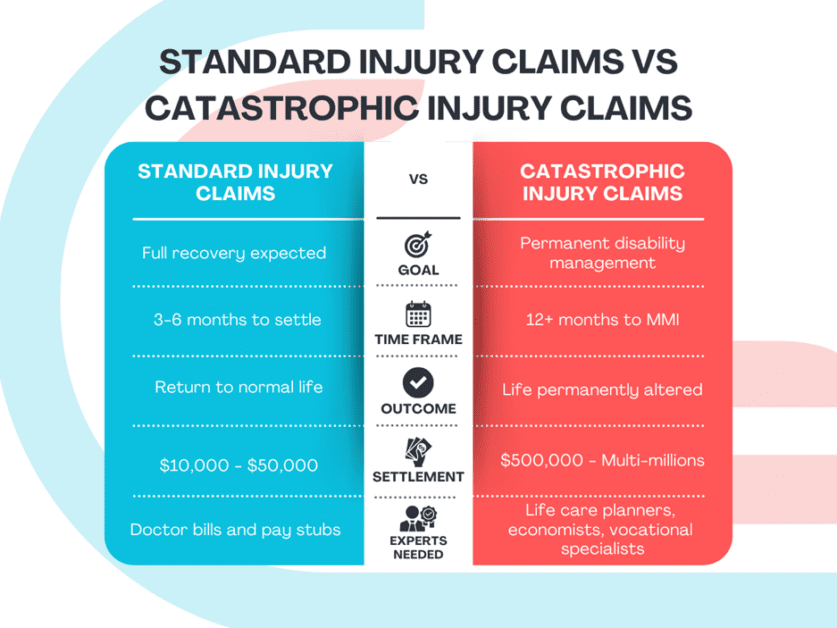

The line between standard and catastrophic isn’t about how bad something hurts initially. It’s about whether you recover.

Standard personal injury cases involve harm that heals. Someone gets rear-ended, suffers whiplash, goes through physical therapy for a few months, and gets back to normal life. There are medical bills. Maybe they miss some work. But recovery happens. Life returns to what it was before.

Catastrophic injuries don’t work that way. These cause permanent changes. Spinal cord damage that leaves someone paralyzed. Traumatic brain injuries that affect cognitive function for life.

Each year, over 80,000 Americans experience permanent disability from traumatic brain injuries alone. Severe burns across major portions of the body. Amputations. The person reaches a point where doctors say they’ve improved as much as they’re going to, but they’ll never get back to where they were before the accident.

Looking Backward vs. Looking Forward

In a standard personal injury case, you add up what already happened. The medical bills you paid. The wages you lost while recovering. Pain and suffering for the months you spent healing. Everything looks backward.

Catastrophic injury cases force you to look forward. The most important numbers aren’t what you’ve already spent; they’re what you’ll spend for the next 30, 40, or 50 years. What kind of medical care will you need a decade from now? Will your home need modifications as mobility gets worse? How does permanent disability affect lifetime earnings?

This forward-looking calculation requires different experts. Life care planners map out every piece of medical equipment, every therapy session, every home modification you’ll need from now until the end of your life.

Economic experts calculate how medical costs will inflate over time. Vocational experts explain how the injury eliminates your ability to work in your field and what that means for your earning capacity over decades.

Standard claims don’t need this. Your doctor bills and pay stubs tell the story.

The Evidence Bar Rises

Proving a catastrophic injury case requires more than showing you got hurt. Medical records need to demonstrate permanent impairment, not just current injury. Future treatment needs have to be substantiated by multiple physicians. Independent medical examiners get involved.

Everything gets scrutinized harder because the potential payout justifies aggressive defense.

Insurers approach these cases differently. They question whether injuries really qualify as catastrophic. They look for pre-existing conditions to blame. They argue you can still work in some capacity. You have to prove every element with concrete evidence.

Standard cases get less pushback. When someone breaks their arm on an icy sidewalk, the injury is obvious, the causation is clear, and treatment follows a predictable path. Hiring a personal injury attorney becomes essential when negotiations focus on projecting decades of future needs rather than just compensating for what already happened.

Timeline Differences Matter

You can’t settle a catastrophic injury case too early. Maximum medical improvement might take a year or more to reach. If you settle before you know the full extent of permanent limitations, you’re gambling. The settlement might seem adequate at the time, but five years later when care costs exceed what you received, there’s no going back for more money.

According to research on injuries requiring long-term disability planning, waiting allows medical experts to fully assess permanent impairment and future needs. Standard claims resolve faster because recovery has an endpoint you can see within months. But the pressure to pay mounting bills pushes some catastrophic injury victims into early settlements that prove inadequate later.

Insurance Coverage and Trial Strategy

Standard personal injury claims usually stay within insurance policy limits. A $100,000 auto policy covers most fender benders and soft tissue injuries. Catastrophic cases blow past available coverage quickly. When damages run into millions but the defendant only carries $300,000 in liability insurance, creative strategies become necessary.

Attorneys explore every insurance source—umbrella policies, business liability coverage, homeowner’s insurance. Insurers know catastrophic injury victims need money fast. This creates opportunities for lowball settlement offers.

Attorneys evaluate whether the potential recovery justifies extensive litigation before committing to these complex cases. They have to show they’re genuinely willing to go to trial. Jury verdicts often far exceed what insurers offer, creating negotiating leverage that standard cases never have.